Global solar PV market set for spectacular growth over next 5 years

The installation of solar PV systems on homes, commercial buildings and industrial facilities is set to take off over the next five years, transforming the way electricity is generated and consumed, according to the International Energy Agency’s latest renewable energy market forecast. These applications – known collectively as distributed PV – are the focus of the IEA’s Renewables 2019 market report, which was released today.

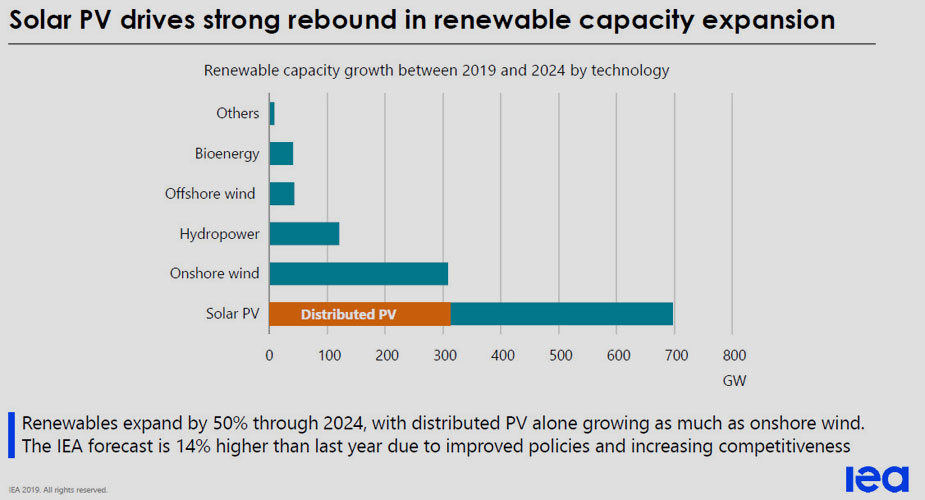

The report forecasts that the world’s total renewable-based power capacity will grow by 50% between 2019 and 2024. This increase of 1,200 gigawatts – equivalent to the current total power capacity of the United States – is driven by cost reductions and concerted government policy efforts. Solar PV accounts for 60% of the rise. The share of renewables in global power generation is set to rise from 26% today to 30% in 2024.

The expected growth comes after renewable capacity additions stalled last year for the first time in almost two decades. The renewed expansion remains well below what is needed to meet global sustainable energy targets, however.

“Renewables are already the world’s second largest source of electricity, but their deployment still needs to accelerate if we are to achieve long-term climate, air quality and energy access goals,” said Dr Fatih Birol, the IEA’s Executive Director.

The report highlights the three main challenges that need to be overcome to speed up the deployment of renewables: policy and regulatory uncertainty, high investment risks and system integration of wind and solar PV.

Distributed PV accounts for almost half of the growth in the overall solar PV market through 2024. Contrary to conventional wisdom, commercial and industrial applications rather than residential uses dominate distributed PV growth, accounting for three-quarters of new installations over the next five years. This is because economies of scale combined with better alignment of PV supply and electricity demand enable more self-consumption and bigger savings on electricity bills in the commercial and industrial sectors.

Still, the number of solar rooftop systems on homes is set to more than double to some 100 million by 2024, with the top markets on a per capita basis that year forecast to be Australia, Belgium, California, the Netherlands and Austria.

“As costs continue to fall, we have a growing incentive to ramp up the deployment of solar PV,” said Dr Birol. The cost of generating electricity from distributed solar PV systems is already below retail electricity prices in most countries. The IEA forecasts that these costs will decline by a further 15% to 35% by 2024, making the technology more attractive and spurring adoption worldwide.

The report warns, however, that important policy and tariff reforms are needed to ensure distributed PV’s growth is sustainable. Unmanaged growth could disrupt electricity markets by raising system costs, challenging the grid integration of renewables and reducing the revenues of network operators. By reforming retail tariffs and adapting policies, utilities and governments can attract investment in distributed PV while also securing enough revenues to pay for fixed network assets and ensuring that the cost burden is allocated fairly among all consumers.

“Distributed PV’s potential is breathtaking, but its development needs to be well managed to balance the different interests of PV system owners, other consumers and energy and distribution companies,” Dr Birol said. “The IEA is ready to advise governments on what is needed to take full advantage of this rapidly emerging technology without jeopardising electricity security.”

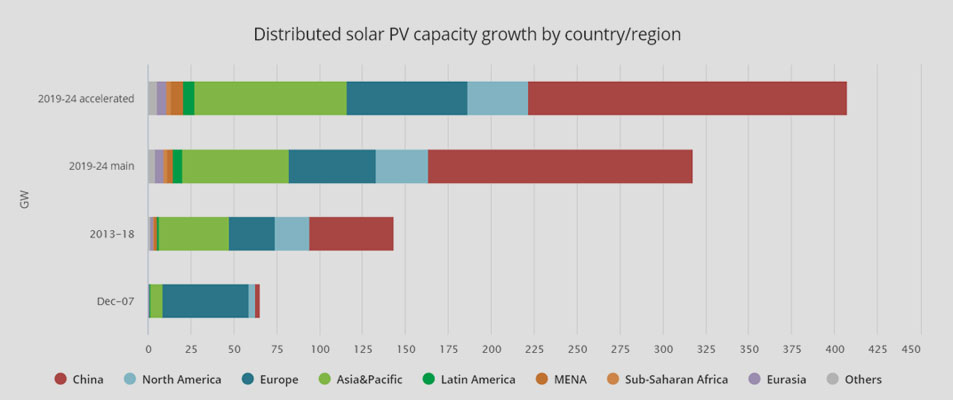

According to the report’s Accelerated Case, improving economics, policy support and more effective regulation could push distributed PV’s global installed capacity above 600 GW by 2024, almost double Japan’s total power capacity today. Yet this accelerated growth is still only 6% of distributed PV’s technical potential based on total available rooftop area.

As in previous years, Renewables 2019 also offers forecasts for all sources of renewable energy. Renewable heat is set to expand by one-fifth between 2019 and 2024, driven by China, the European Union, India and the United States. The heat and power sectors become increasingly interconnected as renewable electricity used for heat rises by more than 40%. But overall, renewable heat potential remains vastly underexploited. The share of renewables in total heat demand is forecast to remain below 12% in 2024, calling for more ambitious targets and stronger policy support.

Biofuels currently represent some 90% of renewable energy in transport and their use is set to increase by 25% over the next five years. Growth is dominated by Asia, particularly China, and is driven by energy security and air pollution concerns. Despite the rapid expansion of electric vehicles, renewable electricity only accounts for one-tenth of renewable energy consumption in transport in 2024. And the share of renewables in total transport fuel demand still remains below 5%. The Accelerated Case sees renewables in transport growing by an additional 20% through 2024 on the assumption of higher quota levels and enhanced policy support that opens new markets in aviation and marine transport.