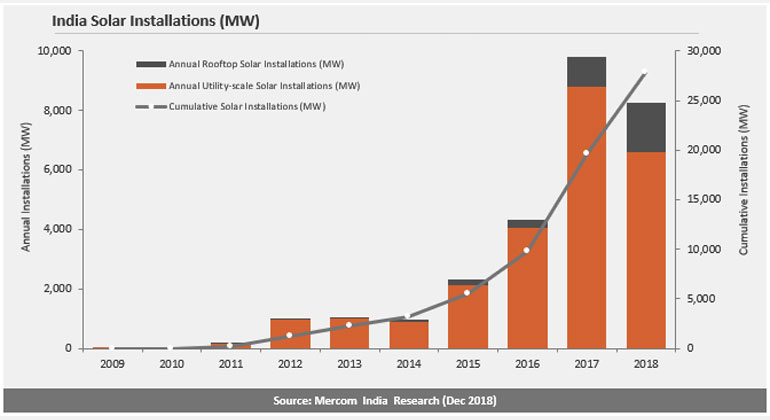

India Installs 8.3 GW of Solar in 2018

The Indian solar market installed 8,263 MW in 2018, down 15.5 percent compared to 9,782 MW in 2017 as the safeguard duty, GST issues, and land and transmission issues took a toll on the large-scale installations, according to Mercom India Research’s newly released Q4 & Annual 2018 India Solar Market Update. Rooftop solar meanwhile had an impressive year.

Q4 2018 installations added to 1,638 MW, up three percent quarter-over-quarter from the 1,589 MW installed during Q3 2018. Installations were down about 52 percent year-over-year (YoY) compared to 2,491 MW installed in Q4 2017.

- “To succeed in the Indian solar market, companies need to play the long game. For the first time in India’s history, solar made up over 50 percent of new power capacity in 2018. We will continue to see a steady shift toward solar as prices continue to drop. This is going to be the new normal as coal plants continue to shutter,” commented Raj Prabhu, CEO and co-founder of Mercom Capital Group.

Rooftop installations in 2018 totaled 1,655 MW a strong 66 percent year-over-year growth. Cumulative rooftop solar installations have reached 3,260 MW and still only make up 12 percent of the total solar installations in the country. In terms of annual growth, rooftop solar continues to be a bright spot, as commercial and industrial entities see rooftop solar as a viable way to combat higher power tariffs. However, Financing rooftop installations could be a challenge in 2019 as Indian banks face a liquidity crunch with many banks hitting the exposure limits to the power sector.

Karnataka topped the list of states with newly added large-scale solar capacity in 2018 followed by Rajasthan, Andhra Pradesh, Tamil Nadu, and Maharashtra. Together these five states accounted for 81 percent of large-scale installations in the year.

- The report found that, “Solar parks continue to face issues in providing clearly demarcated ready land for project development, causing undue delays and pressure on the developers who end up having a shorter timeline to complete the project and the fear of having to pay penalties due to no fault of their own. Government agencies have continued to tender and auction without making sure land, and transmission infrastructure are ready, and it is up to the developers to do the necessary due diligence and understand the risk profile before participating in the auctions.”

The market is adjusting to the safeguard duty regime, but much will depend on Chinese solar policy and installation goals going forward. Any increase in installation targets in China will tighten supplies and harden module prices while oversupply and module price declines could result if China decides to pull back on its solar installation targets.

- “Tariff caps and retroactive cancellation of solar auctions have been the biggest concerns in the investment community,” added Prabhu.

Key Highlights from the report:

- India added 8,263 MW in new large-scale and rooftop solar capacity in CY 2018, in line with Mercom’s forecast.

- Of the total installed capacity in 2018, large-scale projects accounted for 6,608 MW (23 percent decline yoy) and rooftop installations came to 1,655 MW (66 percent yoy growth).

- Cumulative installed solar capacity in India reached 27.9 GW at the end of December 2018. Of this, cumulative rooftop solar installations amounted to 3,260 MW.

- Solar accounted for 50.7 percent of the new power capacity in 2018.

- Renewable energy capacity additions continue to increase at a significant pace in India, accounting for approximately 22 percent of India’s power capacity mix cumulatively.

- In 2018, investments in the Indian solar sector was 15 percent lower compared to the previous year.

Get the full report: Mercom India Research’s Q4 & Annual 2018 India Solar Market Update.